State Mandated Retirement Plans

Stay updated on your state's requirements.

Many states require employers to offer retirement benefits. Starting a Human Interest 401(k) can help you comply with legislation and avoid costly penalties.

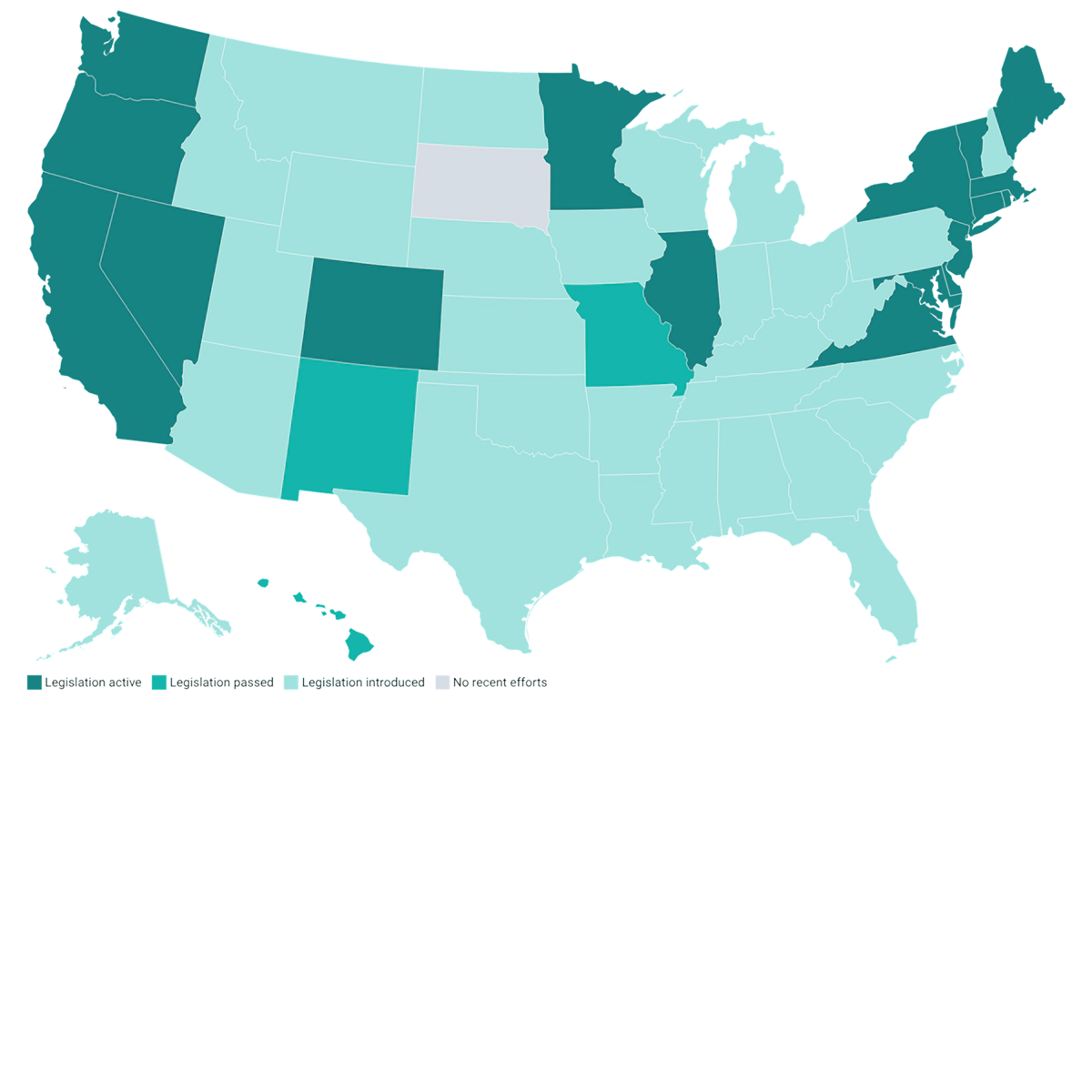

States with active legislation

California - CalSavers

Colorado - Colorado SecureSavings

Connecticut - MyCTSavings

Delaware - Delaware EARNS

Illinois - Illinois Secure Choice

Maine - Maine Retirement Investment Trust (MERIT)

Maryland - Maryland$aves

Massachusetts - Massachusetts CORE Plan

Nevada - Nevada Employee Savings Trust Program

New Jersey - RetireReady NJ

New York - New York Secure Choice Savings Program

Oregon - OregonSaves

Rhode Island - Rhode Island Secure Choice Retirement Savings Program

Vermont - VT Saves

Virginia - RetirePath Virginia

Washington - Washington Saves

States with passed legislation

Hawaii - Hawaii Retirement Savings Program

Minnesota - Minnesota Secure Choice Retirement Program

Missouri - MyRetirement Savings

New Mexico - New Mexico Work & Save and New Mexico Marketplace

Retirement Legislation

State mandate legislation is sweeping the country

More than 20 states have proposed state-mandated retirement plan legislation, and 17 states have active mandated plans.

What are state mandated retirement plans?

What are state mandated retirement plans?

State mandate overview

These programs require employers to provide access to retirement savings options. Employers may enroll their employees in a state-sponsored retirement program—or choose an employer-sponsored plan, such as a Human Interest 401(k) plan. Our 401(k) plans provide a flexible alternative to state-mandated options, ensuring your employees have robust retirement savings opportunities tailored to their needs.

How it works

Most state-mandated retirement programs provide Roth IRAs, with automatic enrollment for employees, which have key differences compared to 401(k) plans. Employees automatically contribute a percentage of wages via payroll deductions unless they opt out or choose their own election. Exemptions may apply to small businesses, new companies, or those already offering qualified retirement plans.

Potential fees & penalties

Employers may face significant penalties for non-compliance. Fines may be charged per eligible employee for failing to offer a retirement plan or properly enroll employees in a qualifying plan. State-sponsored programs may also carry fees that impact employers and employees. Management and recordkeeping fees typically range from 0.5% to 1% of the account balance, while investment fees can vary between 0.1% and 1% annually.

Traits of a typical state program

Limited plan structure

State plans often use Roth IRAs and auto-enroll employees at 3-5% of wages, with opt-out options.

Lower contribution limits

IRA: $7,500/year (under 50), $8,600 (over 50). 401(k): 24,500/year (under 50), $32,500/year (50-59 or 64+), $35,740 (60-63).

Employer roles and fees

Employers aren't required to contribute. Participant fees range from 0.5% to 1% annually.

Portability and management

Accounts are portable, and professional firms manage investment options and compliance.

Investment Options

State plans offer a limited range of investment options, typically including target-date funds, balanced funds, and conservative choices like money market or stable value funds.

Penalties for non-compliance

Employers who fail to comply with state mandates may face annual fines per eligible employee.

Get a smarter retirement solution with Human Interest

Get StartedState mandated retirement plans FAQ