Getting started with retirement savings can be tricky, but there are some steps to take that can make it easier. And while the most important thing to do is save in the first place, figuring out where to begin can feel overwhelming.

Below, we’ll cover what you need to know about different retirement savings tools, including the 401(k), IRA, and more. We’ll also share retirement savings tips that can help you based on your age, relationship status, and more.

Saving wisely: Common retirement savings tools

Let’s start by walking through the most common retirement savings tools and share what you need to know about each of them.

401(k) plans

One of the most common tools to save for retirement is the 401(k), an employer-provided retirement savings plan that comes with tax advantages. We’ll cover the basics below but refer to this guide for more information on how a 401(k) works.

A quick summary: 401(k)s have the highest annual contribution limits of any formal retirement savings plan, the option of an employer match, and numerous tax advantages.

What you need to know about a 401(k)

| How to access | Through your employer |

| How to use it | As an employee at a company that offers a 401(k), you’ll be able to allocate a portion of your paycheck to your 401(k) account. Your employer may add an employer contribution on top of the funds that you put in. |

| Types of 401(k)s | Traditional, Roth |

| Tax advantages | Traditional: Postpone taxes until retirement Roth: Pay taxes upfront so you’ll take money out tax-free in retirement (if certain requirements are met) |

| Annual contribution limit | $23,500 ($31,000 if you're age 50-59 or 64+, $34,750 if you're age 60-63) |

| Associated fees | Vary by plan provider, the types of investments, and whether or not the provider charges any 401(k) transaction fees for specific services, such as taking out a loan, etc. Note: We charge zero 401(k) transaction fees. |

| What else to know | Employer matching contributions do not count toward the annual contribution limit. You can have more than one 401(k) account, even at the same time, but you cannot contribute more than $23,500 ($31,000 if age 50-59 or 64+, $34,750 if age 60-63) per year |

Individual retirement account (IRA)

In contrast to employer-sponsored 401(k) plans, individuals can open an IRA (individual retirement account). Each type of IRA has different restrictions and allowances, so it’ll take some homework to figure out which works for you.

A quick summary: IRAs come with tax advantages and can be opened by individuals, but you cannot contribute as much per year as you can with a 401(k).

| How to access | An individual can open an IRA through a bank, brokerage, investment firm, etc. |

| How to use it | You can put money from any source into an IRA. It’s not connected to your payroll. You can put funds in at any time up to the annual contribution limit. |

| Types of IRAs | Traditional, Roth, SEP, SIMPLE |

| Tax advantages | Traditional: Postpone taxes until retirement Roth: Pay taxes upfront so you’ll take money out tax-free in retirement SEP: Works like a traditional IRA, i.e., postpone taxes until retirementSIMPLE: Works like a traditional IRA, i.e., postpone taxes until retirement |

| Annual contribution limit* | Traditional, Roth: $7,000 ($8,000 if you're age 50+) SEP: Contributions cannot exceed the lesser of 25% of the employee's compensation for the year or $70,000 SIMPLE: $16,500 ($20,000 if you're age 50-59 or 64+, $21,750 if you're age 60-63) |

| Associated fees | Vary by the type of IRA, where the account is held, and possibly by the value of assets in the account. They typically come with an annual or quarterly maintenance fee. |

| What else to know | -SEP and SIMPLE IRAs require specific employment arrangements to be eligible.-Only employers make contributions to SEP IRAs (not employees). -Both a SEP and SIMPLE operate like a traditional IRA in terms of when taxes are paid. They also require an employer to play a role. |

Types of IRAs

Traditional IRA (pre-tax): An IRA where a person can set aside pre-tax money.

Roth IRA (post-tax): An IRA where a person can set aside after-tax income up to a specified amount each year. Both earnings on the account and withdrawals after age 59½ are tax-free. If you have a certain income, you may be restricted in how much you can contribute to a Roth IRA.

SEP IRA (Simplified Employee Pension IRA): A SEP IRA works like a traditional IRA, including contributions, deferred taxes, etc. Only employers can contribute to a SEP IRA.

SIMPLE IRA (Savings Incentive Match Plan for Employees): A SIMPLE IRA is available to employers with 100 or fewer employees and for self-employed individuals.

Brokerage accounts

A brokerage account is an investment account where you can own investment products like stocks, bonds, mutual funds, and more. While many people use brokerage accounts to save for retirement, they aren’t designed specifically for long-term investing.

A quick summary: Brokerage accounts have very few restrictions, but don’t come with built-in tax advantages like a 401(k) or IRA.

What you need to know about a brokerage account

| How to access | An individual can open a brokerage account; some have a minimum investment required |

| How to use it | Most are relatively easy to open, but using them may require more effort. Many are tailored for savvy investors to direct themselves, including choosing their own investments and assembling them into a portfolio. Be sure to find one aligned with your assets (some require a minimum level of assets), your level of investing experience, and the level of control you want to have (e.g. do it for me vs. let me do it myself). |

| Types of brokerage accounts | N/A |

| Tax advantages | N/A - You’ll have to pay capital gains taxes on any growth. |

| Annual contribution limit | None |

| Associated fees | Varied. There may be fees associated with specific investments and for conducting trades. A quarterly or annual account maintenance fee is also typical. |

| What else to know | Features available in brokerage accounts vary, including investments, assets, fees, and product interface.You’ll pay capital gains taxes on any growth (each year as you file income taxes). |

Other retirement savings tools and options

While the above are some of the most common tools people use to save for retirement, there are other options. We’ll cover those briefly and then review some pros and cons.

Real estate: Whether you purchase a property to generate a steady stream of rental income or choose real estate-focused investments, such as Real Estate Investment Trusts (aka REITs), many people are interested in learning more about how real estate could play a role in saving for retirement. Purchasing an investment property is a significant cost, so it may not be an option for everyone. REITs are more accessible and can often be accessed through a 401(k), IRA, or brokerage account, as well as through specialty investing companies. Human Interest includes index funds from a number of leading investment companies that invests in REITs in our Model Portfolios to provide participants exposure and access.¹

Checking/savings accounts: While these accounts can be easy to start and maintain, and often come with minimal fees, they’re not designed to help your money grow. The interest paid on money in a savings account may be at, or below, the rate of inflation, so your money may struggle to keep up with inflation.

Family inheritance: There’s a lot of talk about the windfall that may pass to Gen X and Millennials as Boomers pass on their wealth to the next generation. However, there are a lot of pieces to navigate. Timing may be unknown, the amount may vary widely based on your older loved one’s health and life expectancy, and taxes can be difficult to navigate. This makes relying on a family inheritance a less reliable strategy for funding retirement.

Selling a business: Many business owners may sell their businesses to generate money for retirement. Determining when to sell can be challenging and, in some markets, finding a buyer may be another challenge.

Working during retirement: For many, retirement is no longer the immediate transition from full-time work to full-time leisure. In what we’ve dubbed “pretirement,” Human Interest found that 69% of survey respondents believe retirement is a gradual change away from full-time paid work. More than 90% of workers are open to switching fields or jobs during this stage, with nearly half saying they want to volunteer.

In all likelihood, you may use a mix of the retirement savings tools out there to build up your funds for retirement. Here are some pros and cons of various retirement savings tools:

Here are some pros and cons of various retirement savings tools:

| Type of retirement savings tool | Pros | Cons |

|---|---|---|

| Employer-sponsored retirement plans, like 401(k)s | Higher contribution limits vs. IRAs | Requires access through an employer |

| Checking/savings accounts | Easy access | Lower opportunity for long-term growth |

| IRAs | Easy access | Lower contribution limits per year vs. a 401(k) |

| Employment income in retirement | Keeps pace with inflation; other perks (e.g., social interaction; mental stimulation) | Requires maintaining health and keeping a job |

| Real estate | Has predictable long-term growth historically | High barrier to entry; ongoing maintenance costs |

| Family inheritance | Often one lump sum with the potential to turn into an income stream | Requires navigating complicated IRS tax rules |

Retirement savings tips

No matter how you plan to fund your retirement, some general rules of thumb can benefit most savers. Here are some retirement savings tips you can follow.

1. Start now

One of the biggest money mistakes people make in their 20s or 30s is failing to harness the power of compound growth, one of the most powerful tools in your retirement savings arsenal and the easiest to leverage. All you have to do is start. The sooner, the better.

What is compound growth?

When you deposit any type of investment account, that sum can grow. The average return of the S&P 500, assuming reinvested dividends, over the last 50 years is about 10.5%.² If you were to contribute $39 per biweekly paycheck, here’s what that could look like if you retire at age 65:

| If you start saving at age...* | 20 | 30 | 40 | 50 | 60 |

|---|---|---|---|---|---|

| Balance at 65 | $322,126 | $152,828 | $68,678 | $26,851 | $6,061 |

*Assumes 7% forecasted long-term annual return of a 60/40 equity-to-fixed income portfolio, according to Vanguard’s projections. Past performance, including hypothetical performance, is not a guarantee of future results. See below for more information.³

Want to try? Here’s a retirement calculator you can use to model different scenarios.

2. Contribute enough to max out your employer match

If your employer offers an employer match—a portion of the money they put into your 401(k) for each dollar you contribute yourself—then try to make sure to contribute enough to get the max match and not leave anything on the table.

Note: An employer match does not count against the annual contribution limit you can put in as an individual. The annual contribution limit is $23,500. Any amount your employer contributes does NOT count towards the $23,500.

3. Use a Roth 401(k)

Roth accounts are often advised for younger savers because they’re likely to be in a lower tax bracket now than in the future. That way, you can pay a lower tax rate now—and then, at retirement, you can withdraw money from your Roth 401(k) tax-free (if certain requirements are met).

Note: If your employer offers a match, they’ll be treated as pre-tax contributions (i.e., be taxed upon withdrawal at retirement).

4. Consider making both pre-tax and post-contributions

If you’re not sure which will work best for you, you can hedge your bets by contributing to both a traditional (pre-tax) and a Roth (post-tax) 401(k). Most Human Interest plans offer both. You can even contribute to both simultaneously, though you cannot exceed the $23,500 annual contribution limit between the two.

Retirement savings tips for those over 50 years old

1. Use catch-up contributions

Congratulations! You can accelerate your retirement savings in the decade or two leading up to retirement. The IRS has created special catch-up contribution paths allowing people aged 50 and older to use higher contribution limits, with an additional enhanced catch-up provision for those aged 60-63.

How catch-up contributions help savers age 50+ to accelerate building up their nest egg:

| 401(k) | IRA | |

|---|---|---|

| Age <50 | $23,500 | $7,000 |

| Age 50-59 & 64+ | $31,000 | $8,000 |

| Age 60-63 | $34,750 | $8,000 |

| Total over 10 years* | $235,000-$347,500* | $70,000-$80,000 |

*Assumes the annual contribution limit does not change during those ten years.

2. Start with the most tax-advantaged tools first

You may need to review the suite that your employer offers, but here’s a quick overview of the tax advantages that come with different retirement savings tools:

HSA: Health Savings Accounts are the most tax-advantaged type of account you can save in 1) Your contributions are pre-tax, 2) You can invest the funds, which means any growth is tax-free, and, 3) You can take the funds out at retirement tax-free, so long as you spend that money on eligible health expenses. If you’re age 55+, you can contribute an extra $1,000 here over the annual $4,300 individual limit ($8,550 family limit). You must also be enrolled in a High Deductible Health Plan to be eligible. Read more here.

401(k): Whether it’s a Traditional 401(k) or a Roth 401(k), they both come with tax advantages. (Note: a 403(b) and or 457(b) have similar tax advantages.)

Traditional: Contributions are set aside before federal and state income taxes are withheld. Because this will lower your take-home pay, i.e., your taxable income, you’ll pay less in income tax today. You’ll defer taxes until retirement, when you may be in a lower tax bracket.

Roth: With a Roth, you pay taxes now, but your investments - and any earnings - grow tax-free. That means you can take them out in retirement without any additional taxes (provided you hold your account for at least five years and are at least 59 ½).

IRA: You can also look to an IRA (traditional, Roth, or both) to supplement your retirement savings. Contributions may be deductible on your tax return, and any earnings can potentially grow tax-deferred until you withdraw them in retirement.

Note: There are other tax-advantaged accounts available, though the ones listed above are the primary ones to save for retirement (versus a 529 or ESA, for example, which are tax-advantaged accounts to help you save for an education).

Retirement savings tips for those with low savings

1. Start saving as much as you can

Compound interest refers to the returns on investments in your account that are reinvested and generate returns of their own. The sooner you get started, the sooner you can take advantage of compounding growth. And the sooner you begin saving for retirement, the longer the power of compounding can help you to grow your savings.

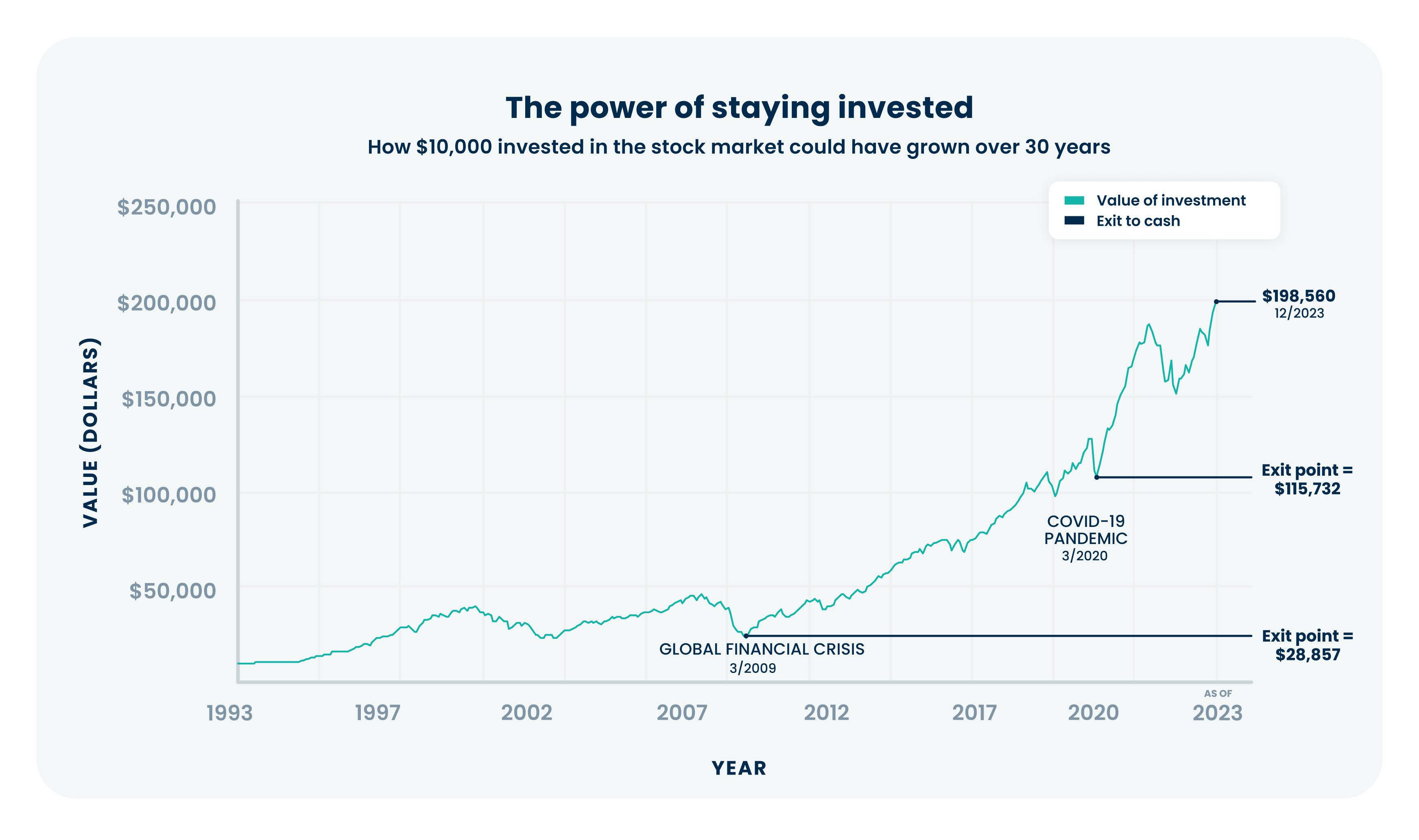

Let's look at a chart that shows how $10,000 could have grown over 30 years from 1992 until 2022. The chart has some ups and downs—which is normal because the market changes—but if you had kept your money invested throughout this period, your $10,000 investment could have grown to over $173,000 by the end of 2022. But let's say you had decided to take all your money out of the market in 2009 amidst the financial crisis. Your investment would have been worth only about $29,000 at that time. Time in the market can often beat timing the market.

Past performance, including hypothetical performance, is no guarantee of future results. Investing is subject to risk, including the risk of loss. S&P data © 2023 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with an actual portfolio. Chart is for illustrative purposes only. See more information below.⁴

2. Move beyond checking/savings

Not all retirement savings tools are created equal. Some provide more advantages than others. Anything that offers the ability to invest opens the opportunity to grow when the market grows, which could be at a pace faster than inflation. Far too many people rely on checking or savings accounts as a primary tool to help them save for retirement. Low interest rates in recent years mean that your money's value may not keep pace with inflation (i.e., it could lose value over time).

3. Keep your money working

What matters is that you set a long-term investment strategy (we can help with that through using any of our model portfolios¹ offered through our built-in digital investment education) and then put your retirement savings on autopilot. It can be tempting to pull money out of the market, especially when you see swings up and down, but we believe it’s important to stick to your strategy and not let emotions dictate your financial decisions.

4. Automate your savings

One of the best features of a 401(k) is that it can help you make it easy to keep putting money away to build up your retirement savings. Each paycheck is an opportunity to add a little bit more.

Good news: It’s easy to start your Human Interest 401(k). In roughly 5 minutes, you can be on your way to help secure your financial future. You can find out more details about your company’s 401(k) plan in the Documents tab at app.humaninterest.com.

Tips to help you accelerate your savings

1. Make sure you’re maxing out your employer match

Does your employer offer a match? If so, are you contributing what you need in order to max out the match? Do the math to figure out what you need to contribute in order to get the max available match. You don’t want to leave any money on the table! To do the math, look up details about the matching formula in the Documents section when you log into app.humaninterest.com.

2. Do a plus 1 (or 2)

Try to increase your contributions by 1% of your annual pay in the next month. If you get a bump in your pay, increase your contribution by another 1-2% on top of that. Here’s what a small increase could look like:

| Annual pay | Contribution rate | Contribution (per pay period)* | Balance at retirement (contributions + Interest*) | |

|---|---|---|---|---|

| Scenario 1 | $50,000 | 4% | $77 | $204,090.25 |

| Scenario 2 | $50,000 | 5% | $96 | $255,112.81 |

| Scenario 3 | $50,000 | 6% | $115 | $306,135.37 |

| Scenario 4 | $50,000 | 7% | $135 | $357,157.93 |

*Rounded; assuming 7% return annually, on average, compounding every biweekly pay period for 30 years. Past performance, including hypothetical performance, is not a guarantee of future results. Data presented in the above chart is hypothetical and assumes no transaction costs or taxes. The chart is for illustrative purposes only and is not indicative of an actual investment.

3. Consider opening an IRA

If you’re feeling behind and you’re able to max out your 401(k), you can look into an IRA where you can squirrel away another $7,000 (pre-tax or post-tax, if you qualify) per year. The tax benefits (i.e., the deduction you could take on your tax return) may be limited if you (and your spouse, if you’re married) have access to a retirement plan through work.

Saving for retirement if you’re in a couple

Planning one retirement is hard enough. Planning for two introduces new complexity: Will you retire at the same time or stagger? Are you optimizing your collective Social Security benefits? What if one of you needs caregiving? This is a topic worthy of a guide itself, but here are a few short considerations to help get you started:

1. Be sure to save for two

You might think: If we both have a 401(k), do we both need to contribute to one? Likely, yes. Default contribution rates, employer matches, etc., are tied to an individual’s earnings rather than a couples. Also, it’s often the case that the role of saving falls to one person in a couple. In that case, they should double down on saving. Why? Dual-earner couples are undersaving and some experts worry that “two-earner couples are in the worst shape for retirement” -- even though they may have two incomes. Dual-income couples with one person contributing to a 401(k) are saving just 5% of their household earnings. Couples with two savers are contributing 9.3%.

2. Get strategic with Social Security

Couples need to think strategically about when to begin collecting Social Security. You can start as early as age 62, but doing so may lock you in at a lower benefit for life by up to 30 percent. It might make sense for the older spouse to delay taking Social Security for a few years, because each month you postpone taking Social Security benefits past Full Retirement Age (varies by the year you were born) up to age 70, you will earn delayed retirement credits which will result in higher monthly benefit payments to you.

3. Have a conversation about caregiving, just in case

The top reason that people leave the workforce before their intended retirement age is for health reasons -- not necessarily their own. Instead, they, especially women, are prone to find themselves retiring earlier than planned. The impact wouldn’t just affect a household’s income today but can trickle down into the future, through reduced contributions to retirement plans and Social Security benefits.

Saving for retirement if you’re divorced

1. Watch out for the QDRO

Typically, any contributions that were put into a 401(k) during the course of the marriage are considered joint property that should be split during a divorce (unless a prenuptial agreement was in place). A Qualified Domestic Relations Order, or QDRO, is required to split apart 401(k)s and similar retirement plans, though is not required for IRAs. What you need to know is they can be expensive to process, running around $500 (or more) -- except if you have a Human Interest plan. A QDRO is just one of more than twenty 401(k) transaction fees we eliminated* in 2020.

2. Know what it means for Social Security

If you are divorced, your ex-spouse can receive benefits based on your record, and that’s true even if you have remarried). The main requirement is that your marriage lasted at least 10 years and that your ex-spouse is still unmarried. Read more on the Social Security Administration website.

Saving for retirement if you’re single

Roughly half of American adults are married today versus 72% in the 1960s and one-quarter of people aged 25-34 are projected to never marry. Because of this, retirement planning for single individuals has become more important. Most retirement advice applies, but special considerations for singles include contingency planning for living alone as well as special strategies when it comes to planning for your health, caregiving, and your estate. It’s about building out a robust safety net.

1. Build your retirement team

If you’re single, you may have friends or loved ones to tap into to help support you in retirement, but you may also need to consult some of the following types of professionals to help with planning:

Geriatric care managers can help with Medicare paperwork, medications, and connections to the healthcare ecosystem, including in-home care, home health aides, and facility-based care

Elder law attorneys can help you organize your estate and document what you want to happen to it after you pass

A CPA can help with tax planning

A Financial Advisor can help with legal, financial, and healthcare decisions

2. Consider contingencies

To help ensure you won’t need to tap into the retirement savings you already have, make sure that you have emergency savings built up and consider obtaining disability insurance coverage, just in case you find yourself needing to take time away from work.

Want more information on saving for retirement? Be sure to refer to our Learning Center for more tips on making the most of your financial future.

Low-cost 401(k) with transparent pricing

Sign up for an affordable and easy-to-manage 401(k).

* Applies to all transaction types. For non-rollover distributions, shipping and handling fees may apply to requests for check issuance and delivery.

Article By

Ronnie CoxAs Investment Director for Human Interest Advisors (HIA), Ronnie’s responsibilities include market and economic commentary, analytical tooling and reporting oversight, and the investment manager search, selection, and monitoring processes. He chairs HIA’s Investment Committee, which sets strategic policy and direction of HIA's investment services.