Key Takeaways

Rhode Island is the twentieth state to require a retirement program for private-sector employers.

Rhode Island Secure Choice Retirement Savings Program offers an auto-enroll IRA option.

However, you have options to comply with state regulations, including offering a 401(k) plan.

In the US, financial security is a growing concern. Recent data indicates that the number of workers in the labor market over the age of 75 is expected to nearly double in the next decade. This is alarming, considering that one out of every five households aged 55-64 has less than $100,000 in total wealth and no defined benefit retirement plan, according to Federal Reserve Board data.

State-mandated retirement programs have become a popular solution to provide a safety net for the millions of workers lacking access to employer-sponsored retirement savings options. Studies have demonstrated that employees are 15 times more likely to save for retirement if their employer offers a plan of some sort.

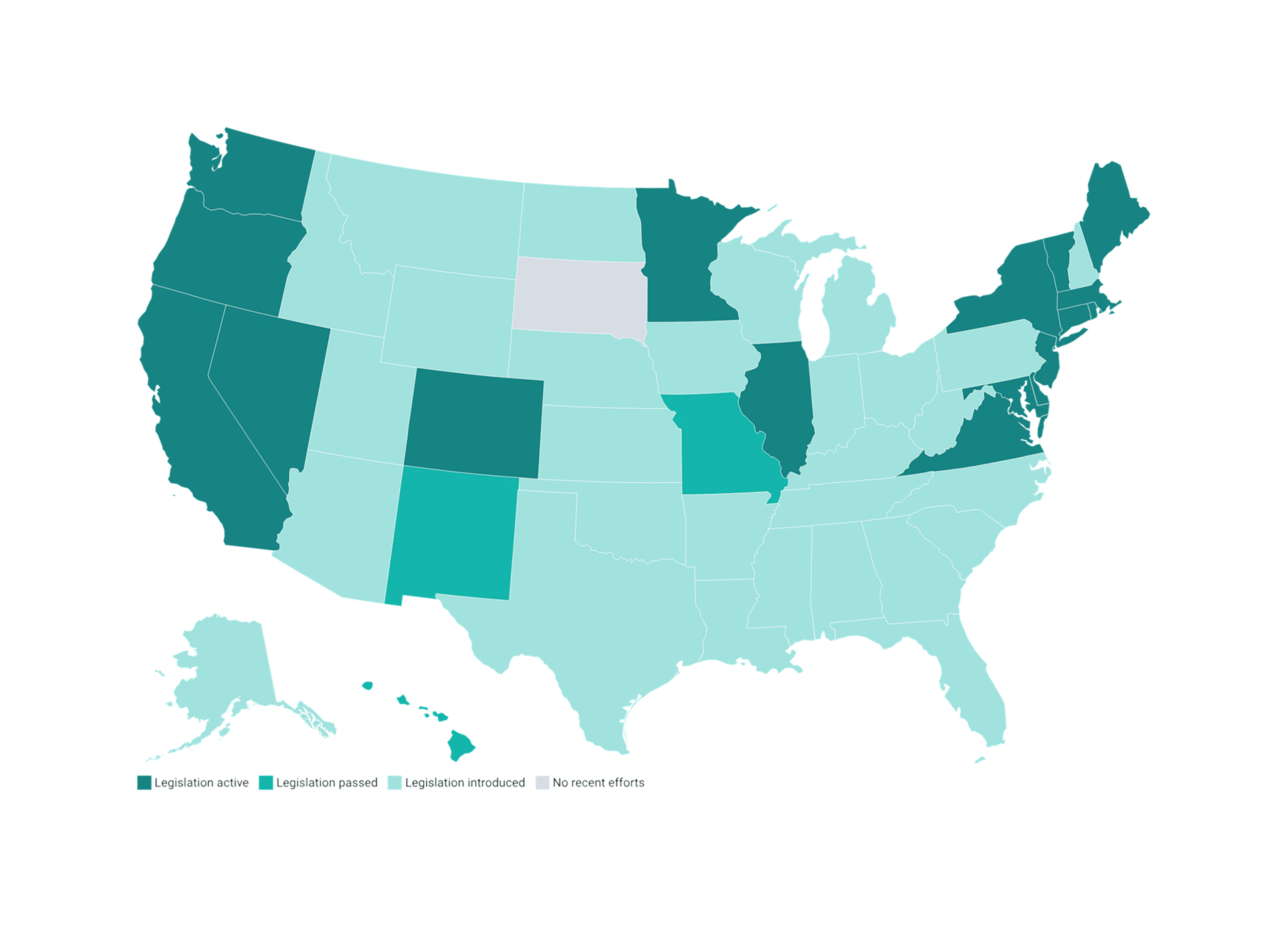

Rhode Island is the latest state to mandate a retirement savings program. Similar retirement programs have been enacted in California, Colorado, Connecticut, Delaware, Hawaii, Illinois, Maine, Maryland, Minnesota, Nevada, New Jersey, New York, Oregon, Vermont, Virginia, and Washington.

What is the Rhode Island Secure Choice Retirement Savings Program?

After several failed attempts over the past few years, Rhode Island passed legislation (2024-S 2045aa, 2024-H 7127aa) in June, establishing the Rhode Island Secure Choice program. It targets part-time and small business employees and aims to bridge the retirement gap for underserved working populations.

The program is based around an automatic enrollment individual retirement account (IRA), which could boost participation rates by simplifying the saving process. Employees contribute through payroll deductions, fostering regular savings without manual deposits. Additionally, accounts are portable, allowing workers to retain their savings when changing jobs—an important benefit for those in high-turnover industries.

This is great news for the approximately 189,000 private-sector employees in Rhode Island without plans. The legislation awaits the governor’s signature.

How does the Rhode Island Secure Choice Retirement Savings Program work?

Under the plan, private-sector employers in Rhode Island with five or more employees will be required to offer their employees a qualified retirement plan or opt into the state-run program.

Per the legislation, the contributions will be made to the program through automatic payroll deductions and the funds will be invested into a default investment or the participant’s choice. The program will be effective for all eligible employers within 36 months of program enrollment, following a phased implementation period.

Under the terms of the bill:

All eligible employees are enrolled in the program unless they opt out.

Employees can opt out by noting it on an opt-out form.

Employers are not liable for an employee's decision to participate or opt out, or for the investment decisions of employees.

Additionally, employers that provide an employer-sponsored retirement plan, such as a 401(k), 403(b), 457(b), SEP plan, SIMPLE plan, or automatic enrollment payroll deduction IRA, are exempt from the program requirements.

Benefits for employers and employees:

The Rhode Island Secure Choice Retirement Savings Program offers substantial benefits for both employees and employers, making it a valuable initiative for all parties involved.

For employees:

Automatic enrollment via payroll deduction with the option to opt out or change contributions at any time.

Contributions are deposited into a post-tax IRA.

The IRA moves with workers if they change jobs.

For employers:

The program is provided at no cost.

Setup is simple; businesses enroll workers and process payroll deductions without being plan sponsors or legally liable for the accounts.

Reporting and administration are handled by a financial services firm hired and overseen by the state.

Offering a retirement savings benefit helps small businesses recruit and retain workers.

Any employer can start its own plan, such as a 401(k), at any time and replace the state program.

What businesses qualify for the Rhode Island retirement savings program?

Employers must determine eligibility for the Rhode Island Secure Choice Retirement Savings Program. The legislation defines which businesses must participate, focusing on private-sector entities with five or more employees and excluding governmental and municipal organizations.

Under the legislation, an “eligible employer”:

Is a person or entity engaged in a business, industry, profession, trade, or other enterprise in the state.

Includes both for-profit and non-profit organizations.

Excludes the federal government, the state, any municipal corporation, or any of the state's units or instrumentalities, with five or more employees.

Retirement planning can be more accessible than you think

For small business owners, providing employees with a retirement savings plan doesn’t need to wait until your state mandates one. Human Interest offers affordable, streamlined plans that make it easy for employers of all sizes to provide a retirement benefit. Contact us today to learn more.

Article By

Trenton ReedTrenton Reed is the Manager of Content Strategy at Human Interest. He has over a decade of experience writing for Fortune 500 and SMB companies across finance, technology, and other verticals.