In times past, both employers and employees viewed a pension or retirement plan as a given part of their business arrangement. In exchange for years of service, the convention held that a worker could expect years of financial security—supported partly by their employer—during retirement. Times have changed. According to recent BLS data, roughly one-third of private-sector employees are not offered any retirement savings plan through their employers.

We know that people tend to save more when these plans are offered, and we expect that our fragile Social Security will offer only, at best, a supplement to people’s personal savings. These and many other factors contribute to what is known as the retirement crisis, which extends beyond what is missing from the savings accounts of the American workforce.

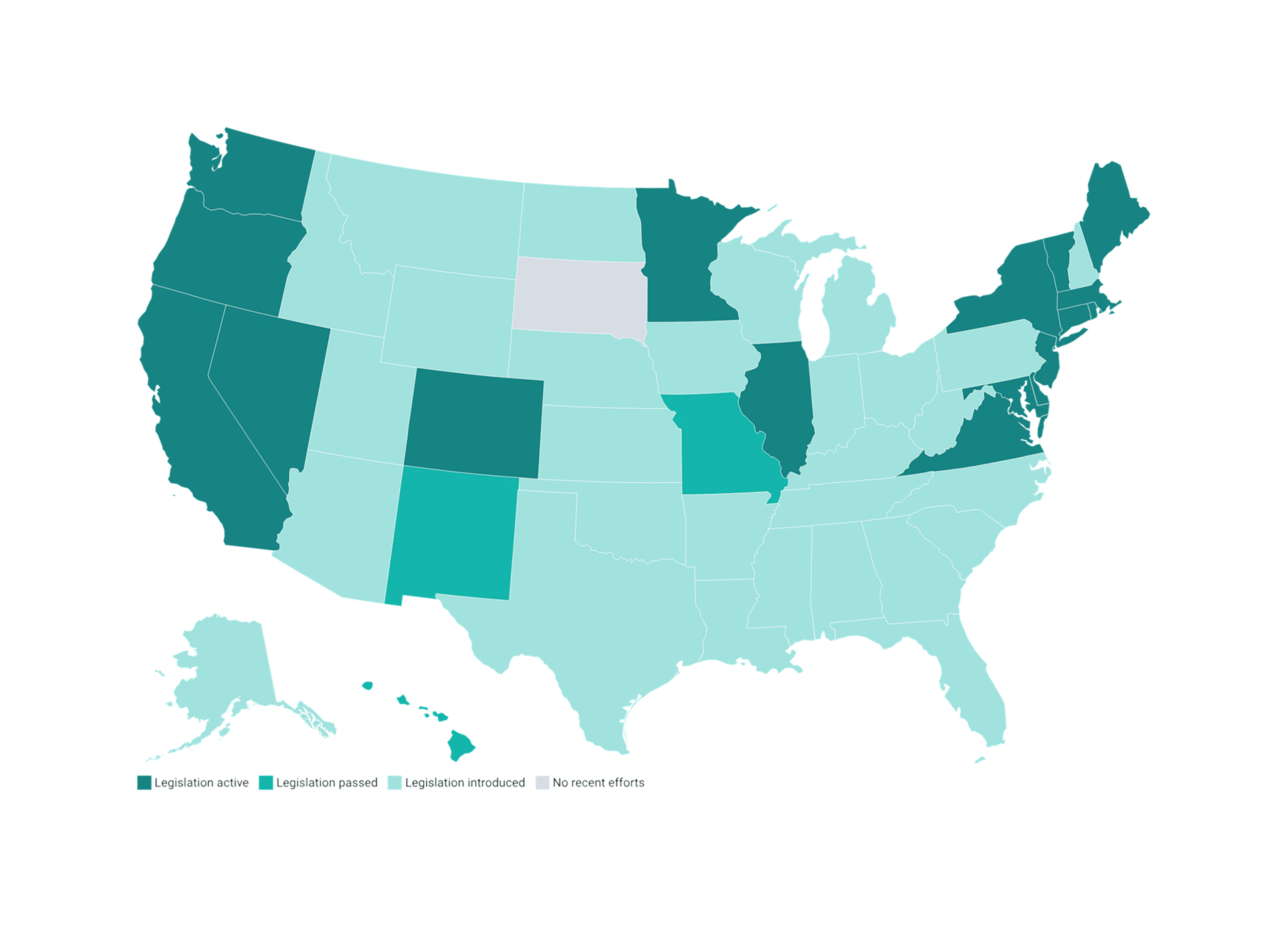

Now, many states have passed laws that require private-sector employers to offer retirement plans to their employees—and Arizona may be the next state to join the trend. This article will cover the fundamentals of Arizona’s pursuit of a solution to the retirement crisis. We’ll highlight what Arizona business owners need to know right now to prepare for what’s next.

Arizona and the retirement crisis

Arizona is known as a great place to retire. It’s sunny, the scenery is gorgeous, and the home prices are reasonable. But the state is also home to a staggering number of retirement-age people who, as a broad demographic, simply don’t have enough saved for retirement, which is in line with a 2015 paper showing that only about half of the state’s workforce was offered a retirement plan. Lawmakers are betting on a state-run retirement plan to fix this, so let’s dig into the solution.

What we know about Arizona’s retirement bill?

If the Arizona Secure Choice Retirement Savings Trust Act (HB 2063, or Arizona Secure Choice Retirement Savings Program) is signed into law, access to a retirement plan will be required. But don’t let the fact that this bill was introduced in 2014 lead you to believe it is forgotten. This bill could be swept up with the momentum of other states making similar moves, and before long, Arizona business owners may be operating under a new rulebook.

Until then, Arizona business owners should take note of what we know so far.

HB2063 will require private-sector employers with five or more employees that have been in operation for at least two years and that don’t already offer a qualified employer-provided retirement plan to make the state’s program available to their employees.

Employee contributions would be deposited in an IRA for the employee at a 3% default contribution rate unless the employee opts out.

Employers must have an annual open enrollment period. .. Employees—including those who previously opted out—will be automatically enrolled unless they opt out. The employer may allow employees who have opted out an opportunity to enroll at any time or they may require them to wait until the annual open enrollment period to enroll.

The following is also outlined in the bill—but with the official start date as yet unknown, these guidelines are missing context:

Three months after the bill is signed into law: Eligible employers with more than 100 employees must participate in the program.

Six months after the bill is signed into law: Eligible employers with more than 50 employees must participate in the program.

Nine months after the bill is signed into law: “All other” eligible employers must participate in the program

For now, it’s time to wait until more details about the bill are available—including any launch dates and deadlines. And while it’s unknown what the future will bring, business owners can get ahead of what’s on the horizon by digging into their options.

Employer-sponsored 401(k) plans vs. state-run IRA

Small and medium-sized business owners could be the most impacted by this change and would be wise to familiarize themselves with their options. According to the current version of the bill, employers may offer the state run option or any type of qualified employer-sponsored retirement plan, including a defined benefit plan such as a 401(k).

The ins and outs of this decision will be particular to the people making them, and to the businesses they own or represent. As the fine print comes into focus, we recommend getting familiar with all the available information.

Here are the two most common reasons companies choose the 401(k):

Tax advantages: Employers and employees both enjoy tremendous tax advantages when using 401(k) plans. Employers may match employee contributions or provide a profit sharing contribution, which may be deductible on an employer’s federal income tax return. Plus, 401(k) plans also allow for higher contribution limits for participating employees when compared to IRA plans.

Simplicity and cost-effectiveness: The 401(k) can be affordable and easy to run, due to features like payroll integration, which can help reduce the manual work of plan administration.

Another thing to consider: this law could help inspire an allegiance between employers and their worker's lifetime financial security. This shift in mindset may be related to the recalibration of the relationship between the American workforce and its employers, and the associated difficulties some companies have finding and keeping staff. To compete for top talent, companies are offering perks—including retirement benefits. To that extent, it may come as no surprise to learn that, after health insurance, the 401(k) is the second-most desired employee benefit, according to a survey from March 2022 conducted by OnePoll, paid for by Human Interest.

While the details of Arizona’s state-provided options are still in the air, it’s possible to get ahead of the curve today with a 401(k) plan. Let Human Interest help you weigh your options.

*Alison Hunter is an independent contractor commissioned by Human Interest to help contribute to this article.

Low-cost 401(k) with transparent pricing

Sign up for an affordable and easy-to-manage 401(k).

Article By

The Human Interest TeamWe believe that everyone deserves access to a secure financial future, which is why we make it easy to provide a 401(k) to your employees. Human Interest offers a low-cost 401(k) with automated administration, built-in investment education, and integration with leading payroll providers.