While there are many 401(k) tax advantages, some workers still feel that they would be better off by delaying their contributions to a 401(k) plan. This is particularly true for single filers making about $30,000 per year or joint filers pulling a combined $60,000 per year. Knowing it’s critical to start saving for retirement early, Uncle Sam offers qualifying low-to-moderate income workers the Retirement Savings Contributions Credit, better known as the Saver’s Credit, to encourage retirement savings. Let’s review what is this credit, who can qualify for it, and how to claim it.

What is the Saver’s Credit?: Tax deduction vs. Tax credit

The Saver's Credit is also known as the Retirement Savings Contributions Credit. Unlike a tax deduction, which reduces your taxable income, a tax credit reduces your actual tax liability. The Saver’s Credit allows single filers and joint filers to reduce the amount of taxes owed to the IRS by up to $1,000 and $2,000, respectively in 2017. By withholding pre-tax dollars from your paycheck away on your 401(k), you could potentially reduce your federal tax liability to $0.

However, the Saver’s Credit is a non-refundable credit, meaning that it can’t provide you a refund when you don’t owe any taxes.

Who qualifies for the Saver’s Credit?

In 2017, to be eligible for the Saver’s Credit, the person making the contributions to an employer-sponsored 401(k) must meet the following three criteria:

Be age 18 or older;

Not be a full-time student during any part of five calendar months of 2016; and

Not be a dependent on somebody else’s return.

Additionally, your adjusted gross income has to be below $30,751 in 2017. More on this below!

Are all retirement contributions eligible for the credit?

To calculate your credit, you can include your (and your spouse’s) contributions to a traditional 401(k), 403(b), 457 plan, Simple IRA, SEP IRA, traditional IRA, and Roth IRA.

However, any employer contributions to your retirement accounts aren’t considered to be voluntary contributions and don’t qualify for the credit. Contributions made with after-tax dollars to an employer-sponsored 401(k) or Roth 401(k) and any type of rollover contributions aren’t eligible either.

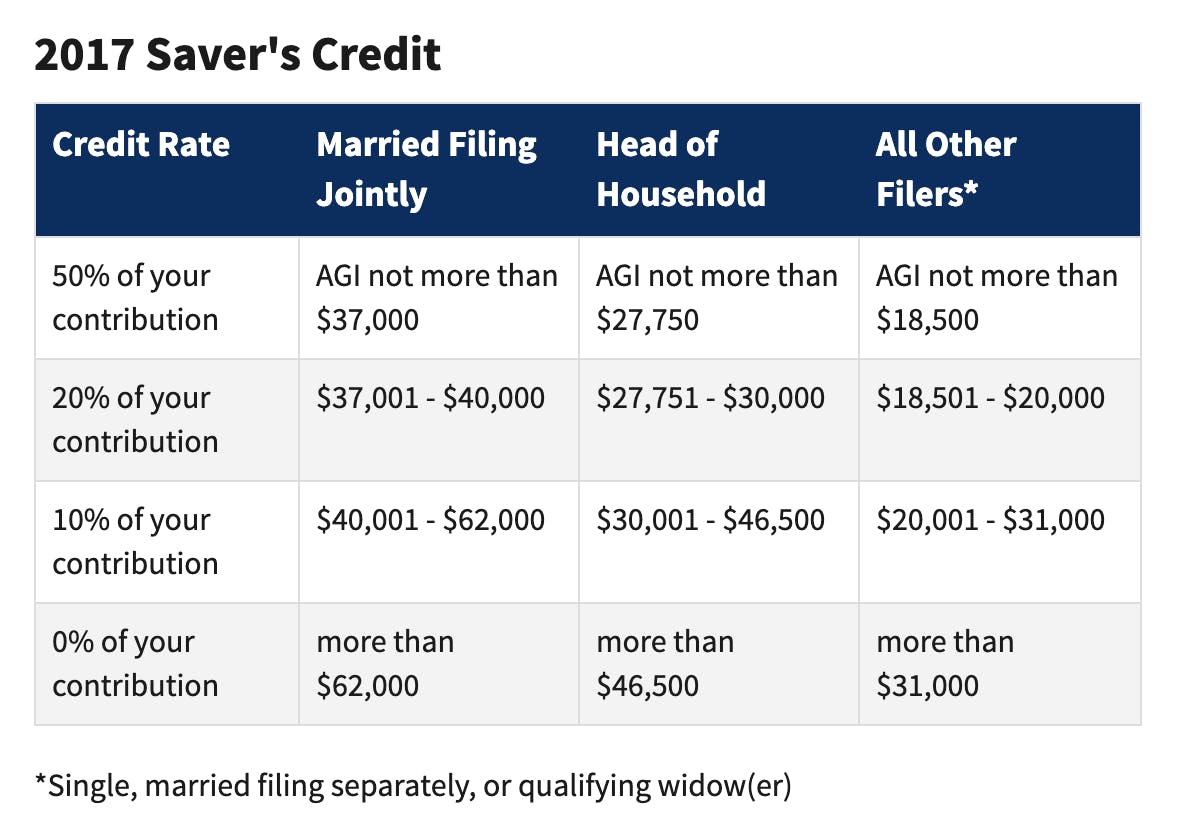

How much is the Saver’s Credit? What are the income limits?

Depending on your adjusted gross income (AGI), you can claim 50%, 20%, or 10% of the first $2,000 ($4,000 if filing jointly) in contributions to your 401(k) or eligible retirement account. Once you hit a certain threshold, your contributions are no longer eligible for this credit.

You can find your AGI on:

Line 4 of

Line 21 of

Line 37 of

Here’s how much you claim as Saver’s Credit in 2017:

What are some examples of workers claiming the Saver’s Credit?

More people than you think are eligible or can become eligible for the Saver’s Credit. Consider the following examples:

John is a parking attendant making the median annual salary of

and contributed $2,000 to his employer-sponsored 401(k). Assuming no other pre-tax deductions, his AGI is $27,906 and he can claim a Saver’s Credit of $200 ($2,000 x 10%).

Lucy finished her college degree in April and didn’t find a job until August. Her new job has an annual salary of $49,200 per year, so she made $20,500 during the five-month period. She contributed $2,000 to her 401(k) and $1,000 to her $1,000 flexible spending account (FSA) during that year. The AGI on her 1040EZ is $17,500 ($20,500 - $2,000 - $1,000), so she can take a credit of $1,000 ($2,000 x 50%).

Mary, who works as an executive assistant, is married and earns $30,000. Mary’s husband, Jack was unemployed for most of the year and only made $7,000 that year. Mary contributed $1,500 to her 401(k). After deducting her 401(k) contribution, their combined AGI shown on their joint return is $35,500 ($30,000 + $7,000 - $1,500). Mary may claim a 50% credit equivalent to $750 ($1,500 x 50%).

Marc and Leslie make $50,000 and $40,000 per year, respectively. Leslie becomes pregnant in February and has to be on bed rest for her pregnancy (a full 9 months). Leslie’s workplace provides temporary disability insurance (TDI) and she’s eligible to receive a benefit of 58% of her usual paycheck for several weeks. Also, she takes maternity leave in December. Marc and Leslie contributed $2,800 and $400, respectively, to their workplace 401(k). By law, Leslie’s TDI benefits aren’t subject to federal or state income taxes and aren’t included in her taxable income. Since their combined AGI is $53,467 ($50,000 + $6,667 - $2,800 - $400), they can take a credit of $320 ($3,200 x 10%).

As you can see from these four scenarios, it really pays to check whether or not you qualify for the Saver’s Credit. Contributing to a retirement account, FSA, HSA, or other types of flexible spending accounts, and receiving income not subject to taxes can also make you eligible for this credit.

Here are some resources on FSA plans:

How do I claim the Saver’s Credit?

If you’re preparing your taxes and find out that your AGI falls within the qualifying thresholds (no more than $30,750 for single filers and heads of household and $61,500 for married joint filers), then file your federal taxes using Form 1040, Form 1040A, or Form 1040NR and attach Form 880, Credit for Qualified Retirement Savings Contributions.

Let’s review what you would fill out on each of the 12 lines of Form 8880:

Line 1

You and your spouse’s contributions to a traditional and Roth IRA (including myRA). Don’t include rollover contributions.

Line 2

Include all pre-tax contributions made to an employer-sponsored 401(k) or other qualified workplace plan, such as a 403(b) or 457 plan. Generally, contributions to your 401(k) plan will show up in box 12 of your W-2 form, with the letter code D.

Line 3

Add lines 1 and 2 and enter the total here.

Line 4

If you or your spouse took any distributions from retirement accounts after 2013 and before Tax Day or the date that you file your return, write them here. Certain distributions will reduce your eligible amount for the Saver’s Credit.

Line 5

Subtract line 4 from line 3. If zero or under, enter 0.

Line 6

In each column, (a) for you and (b) for your spouse, enter the smaller of line 5 or $2,000.

Line 7

If you’re a single filer or head of household, copy the amount from line 6 from column (a).

If you’re a married joint filer, add the amounts from columns (a) and (b) from line 6.

If the amount on line 7 is zero, stop; you can’t take the Saver’s Credit.

Line 8

Enter your AGI. This is amount from your Form 1040, line 38; Form 1040A, line 22; or Form 1040NR, line 37.

Line 9

Using the table provided on line 9, choose the applicable decimal (.5, .2, .1 or .0) based on your AGI from line 8 and your filing status.

If the amount on line 9 is .0, stop; you can’t take the Saver’s Credit.

Line 10

Multiply line 7 by line 9.

Line 11

Use this Credit Limit Worksheet to figure the amount to enter on line 11:

Line 1

Enter the amount from Form 1040, line 47; Form 1040A, line 30; Form 1040NR, line 45.

Line 2

Form 1040 filers: Enter the total of your credits from lines 48 through 50 and Schedule R, line 22. Form 1040A filers: Enter the total of your credits from lines 31 through 33. Form 1040NR filers: Enter the total of your credits from lines 46 and 47

Line 3

Subtract line 2 from line 1. Also enter this amount on Form 8880, line 11. But if zero or less, stop; you cannot take the Saver’s Credit.

Line 12

Input the smaller of line 10 or line 11 here and on Form 1040, line 51; Form 1040A, line 34; or Form 1040NR, line 48.

Now, it’s your turn. Make the most of your retirement contributions by checking every year if you can take the Saver’s Credit on your tax return. Even when you don’t qualify for one year, continue to check year after year. Reducing your tax liability is always a good idea.

Additional resources on personal taxes:

Article By

Damian DavilaDamian Davila is a Honolulu-based writer with an MBA from the University of Hawaii. He enjoys helping people save money and writes about retirement, taxes, debt, and more.